The Group’s risk management framework, which is approved by the Board, supports the achievement of strategic objectives and promotes risk-informed decision-making. The Board is ultimately responsible for establishing and overseeing the Group’s risk management framework which is supported by the Group’s underlying systems, structures, policies, procedures, processes and people.

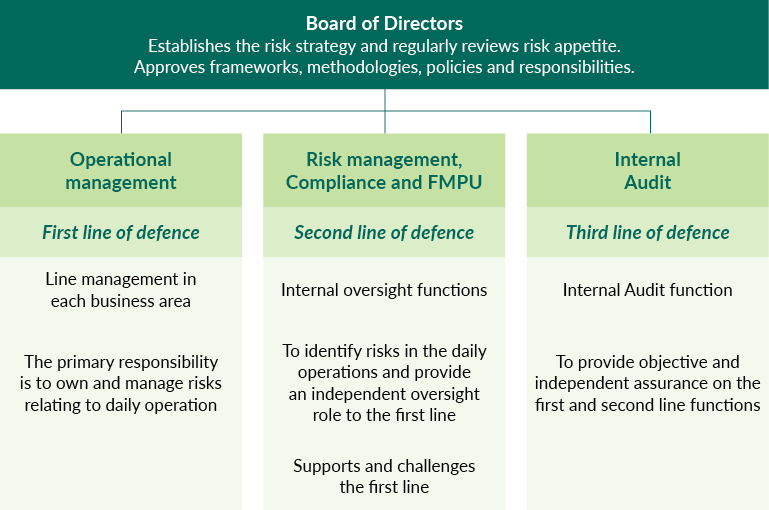

The Group is committed to building and maintaining a sound risk culture. Our risk culture is an important part of our organisational culture It is shaped by our core values, beliefs, knowledge, attitude, and risk awareness across our diverse operations. We leverage the three lines of defence model to build and maintain a strong risk culture.

ASA International has a moderate risk appetite. We strive for a balanced approach, accepting risks associated with investing in microfinance operations in emerging markets while prioritising prudent risk management to safeguard the interests of our clients, investors, and stakeholders. Our commitment to a high level of compliance, strict adherence to well-defined operational procedures, and a focus on sustainable financial inclusion are the basis of our dedication to achieving social economic impact for our clients and generating sustainable financial returns for the Group.

The Group establishes its risk appetite to provide direction and set boundaries for risk management across its microfinance institutions. The Group targets more conservative financial and prudential ratios than required by regulators in the countries of operation while driving compliance with local regulations and laws. The Group also has zero tolerance for any unethical, illegal or unprofessional conduct. The risk appetite assigns tolerance levels based on regulatory expectations, past trends, and forward-looking business projections. The tolerance levels are periodically reviewed and adjusted, if necessary. This dynamic approach ensures that the Group’s risk appetite remains aligned with evolving business conditions and strategic objectives.

Details for the principle risks can be found on pages 42-48 of the 2025 Annual Report. This section should not be regarded as a complete and comprehensive statement of all potential risks and uncertainties faced by the Group but rather those which the Group currently believes may have a significant impact on its performance and future prospects.

Emerging risks present potential threats or uncertainties, often characterised by unpredictability and the potential for significant impact, and may materially affect our risk profile if they occur. These risks are identified through ASA International’s regular risk assessments at Group level and across its entities, as well as through escalation of notable external and internal developments, and are discussed with mitigating actions at ALCO, ExCo and, where required, reported to the Board.

The Group’s performance is closely linked to the political, economic, financial and environmental conditions in the regions in which we operate and our customers conduct business, with the current external environment shaped by significant global events, particularly geopolitical and environmental factors affecting economic stability, regulatory frameworks and business conditions. In 2025, currencies in our countries of operation performed well, and this, combined with close management of foreign exchange risk, was favourable.

Looking ahead to 2026, while demand for loans is expected to remain resilient, there remains a high degree of unpredictability around the duration and scale of the Middle East war and its potential effects on commodity prices, supply chains, economies and credit conditions, and we continue to closely monitor its impact on inflation, local currencies and growth across our markets.

Our operations and portfolios remain exposed to risks arising from political instability, civil unrest and military conflict, which could disrupt operations, pose physical risks to staff and cause damage to assets. During 2025, the Group closely monitored and managed risks in Myanmar, including political and security developments and the impact of the March 2025 earthquake, as well as election-related disruptions in countries of operation, notably Tanzania following the October 2025 general election; however, these events did not have a material impact on the business.

From a climate and environmental perspective, severe storms in the Philippines during the second half of 2025 disrupted branch operations, transport and client activities, while flooding in Sri Lanka in the final quarter affected borrower livelihoods and economic activity; the Group continues to support customers and communities during such events and invest in resilience measures.

During the year, the Group initiated the development of an enhanced risk strategy and risk appetite framework, including a more comprehensive risk taxonomy and guidelines for risk measurement and reporting, designed to provide a holistic, company-wide view of key risks. In parallel, the Group developed a risk evaluation methodology to guide the incorporation of financial and non-financial considerations into risk scoring, supported by Key Risk Indicators (‘KRIs’) to enhance consistency and robustness. Policies will be developed or enhanced, as applicable, to support the management of principal risk areas, with clearly defined ownership and accountability. Implementation is planned for 2026 and is central to preparation for compliance with Provision 29, with further engagement planned for H1 2026.

The first line of defense owns and manages the risks that arise from the Group’s activities and mainly comprises operational staff, such as loan officers and branch managers, responsible for managing risks in daily activities. They ensure compliance with policies, conduct client due diligence to prevent fraud and over indebtedness, and maintain accurate records to minimize errors. Within the first line of defence, Internal controls, like dual approvals, are used to safeguard processes and enhance risk management.

The second line of defence refers to independent control functions, that provide oversight and challenge to the first line risk management processes and decisions. It includes internal oversight functions such as Compliance, Risk Management, and the Fraud and Misappropriation Prevention Unit (‘FMPU’).

The third line of defence is Internal Audit at both the Group level and the microfinance institution level. In addition to regularly performing internal auditing activities, Internal Audit ensures that all units responsible for managing risk are performing their roles effectively and efficiently.